cost of living crisis

The cost of living crisis has become one of the defining economic challenges of the 2020s, reshaping household budgets and national policy debates alike. Inflation, supply chain disruptions, and geopolitical tensions have converged to push essential expenses—housing, food, energy—beyond reach for millions. Unlike cyclical price fluctuations, this crisis reflects deeper structural imbalances in energy markets, wage growth, and public infrastructure.

Households are feeling the squeeze most acutely. A recent study by the Joseph Rowntree Foundation found that over 13 million people in the UK alone are unable to afford basic essentials, with energy and food costs rising at nearly double the rate of wages since 2021. The ripple effects are visible in declining consumer spending, rising debt levels, and growing reliance on food banks. This isn’t just a temporary blip—it’s a long-term erosion of economic security for working families.

The Drivers Behind Rising Costs

Several converging factors have fueled the cost of living crisis. Energy prices surged following Russia’s invasion of Ukraine in 2022, triggering global gas price spikes that pushed household energy bills to record highs. In the UK, the average annual energy bill peaked at over £2,500 in early 2023—more than double pre-pandemic levels. While government support schemes provided temporary relief, they did little to address the underlying volatility in global energy markets.

Food inflation has also played a major role. The UN’s Food and Agriculture Organization reported a 28% increase in global food prices between 2020 and 2023, driven by disrupted supply chains, extreme weather events, and rising fertilizer costs. Domestically, supermarket price wars have done little to offset the burden on consumers, particularly those on lower incomes who spend a larger proportion of their earnings on essentials.

Housing remains a critical pressure point. In many urban areas, rental prices have outpaced wage growth by 300% over the past decade. The average rent in London now consumes over 40% of median income, while social housing waiting lists stretch into years. The result is a generation increasingly locked out of homeownership and facing unstable, often unaffordable, rental conditions.

Who Is Most Affected?

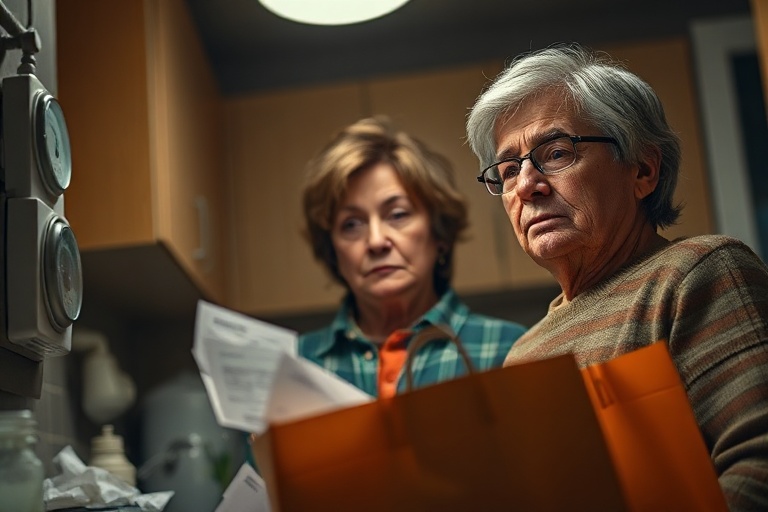

The impact of the cost of living crisis is not evenly distributed. Vulnerable groups—single parents, disabled people, and those in low-paid or insecure employment—are disproportionately affected. A survey by Citizens Advice revealed that 45% of households with disabled members are cutting back on food to afford energy, compared to 28% of non-disabled households. Similarly, renters are three times more likely to report financial distress than mortgage holders.

Young adults face a unique set of challenges. The Resolution Foundation found that people aged 25–34 are spending 35% more on essentials than they did in 2019, with many delaying major life milestones like homebuying or starting families. The crisis has also widened regional inequalities. Areas with lower economic output and higher unemployment—often former industrial towns—are experiencing deeper cuts to essential services and public transport, compounding social exclusion.

Meanwhile, pensioners on fixed incomes are increasingly forced to choose between heating their homes and buying medication. Age UK reports a 22% rise in excess winter deaths since 2019, partly attributed to fuel poverty. The crisis has exposed the fragility of social safety nets that were already stretched thin before the pandemic.

Policy Responses and Their Limitations

Governments have responded with a mix of short-term support and structural reforms. The UK’s Energy Price Guarantee capped bills at £2,500 annually between 2022 and 2024, while the Household Support Fund provided £1 billion to local authorities for emergency assistance. In the EU, member states introduced subsidies for vulnerable households, though these have often been criticized as unsustainable and regressive.

But policy responses have struggled to balance immediate relief with long-term resilience. Energy subsidies, while necessary, have delayed investment in renewable infrastructure and energy efficiency—key levers for reducing future price shocks. Likewise, rent controls and social housing investment remain politically contentious, with some arguing they deter private investment.

There’s also a growing recognition that traditional monetary policy—raising interest rates to curb inflation—can worsen the crisis for indebted households. The Bank of England’s base rate hikes from 0.1% in 2021 to over 5% in 2023 increased mortgage costs for millions, particularly those on variable-rate deals. This highlights a dangerous paradox: fighting inflation can deepen financial hardship for those already struggling.

What Can Be Done? Paths to Resilience

Addressing the cost of living crisis requires a multi-pronged approach that goes beyond emergency aid. First, accelerating the transition to renewable energy could reduce exposure to volatile fossil fuel markets. The International Energy Agency estimates that doubling investment in clean energy could cut global energy bills by $1 trillion annually by 2030. Such a shift would not only stabilize prices but also create jobs in growing sectors.

Second, structural reform in housing is essential. Increasing social housing stock—by 90,000 units per year in the UK alone—could ease rental pressure and reduce homelessness. Rent stabilization policies, like those in Germany, have shown promise in curbing excessive increases without stifling investment.

Third, wage policies must catch up with living costs. A higher real living wage—adjusted annually for inflation—could help workers keep pace with rising expenses. In sectors like social care and hospitality, where wages are already low, government incentives for fair pay could reduce reliance on state benefits.

Finally, financial inclusion initiatives can help households build resilience. Programs offering debt advice, energy efficiency grants, and emergency savings schemes have proven effective in reducing financial stress. Charities like Turn2Us and StepChange report that targeted support can prevent families from falling into crisis.

The cost of living crisis is not just an economic issue—it’s a social one. It threatens to widen inequality, reduce social mobility, and erode public trust in institutions. Without coordinated action across energy, housing, wages, and welfare, the burden will continue to fall on the most vulnerable. The question is no longer whether the crisis will persist, but how society chooses to respond.

Resources and Further Reading

For those seeking support or deeper analysis, the following organizations offer guidance and data:

- Joseph Rowntree Foundation – Research on poverty and inequality

- Citizens Advice – Financial advice and advocacy

- Age UK – Support for older people facing financial hardship

- StepChange – Debt advice and financial education

Understanding the full scope of the crisis means looking beyond headline inflation figures. It requires examining how energy, food, housing, and wages interact to shape daily life. Only by addressing these interconnected pressures can we build an economy that works for everyone—not just in times of stability, but in crisis too.